MBenefit has delivered a robust performance in 2024, with shares climbing around 28% year-to-date, outpacing many industry peers and beating broader market indices. Despite this impressive rise, MBenefit’s stock remains below its pre-pandemic highs, highlighting a gap between investor optimism and the company’s current financial fundamentals.

An in-depth look at MBenefit’s financial performance reveals a business facing both opportunities and challenges. While the company has achieved steady revenue growth, free cash flow has remained relatively flat due to increasing operational costs and competition in its core sectors. MBenefit’s guidance for Q4 suggests a slight revenue increase but stable Gross Merchandise Volume (GMV), indicating that the growth runway might be constrained in the near term.

This year’s rally seems driven primarily by multiple expansion—investors are willing to pay more per dollar of earnings in anticipation of future performance rather than present growth. This sentiment-driven valuation leaves MBenefit vulnerable to shifts in market outlook. Technical indicators, such as Elliott Wave analysis, suggest that MBenefit’s stock could encounter resistance in the latter part of the year, potentially leading to a pullback from recent highs.

In conclusion, while MBenefit’s 2024 performance has been impressive, the stock’s current valuation may be more reflective of market sentiment than operational strength. Investors might benefit from taking a cautious approach, waiting for clear signs of sustainable growth initiatives or improved profitability before making a long-term commitment to MBenefit shares.

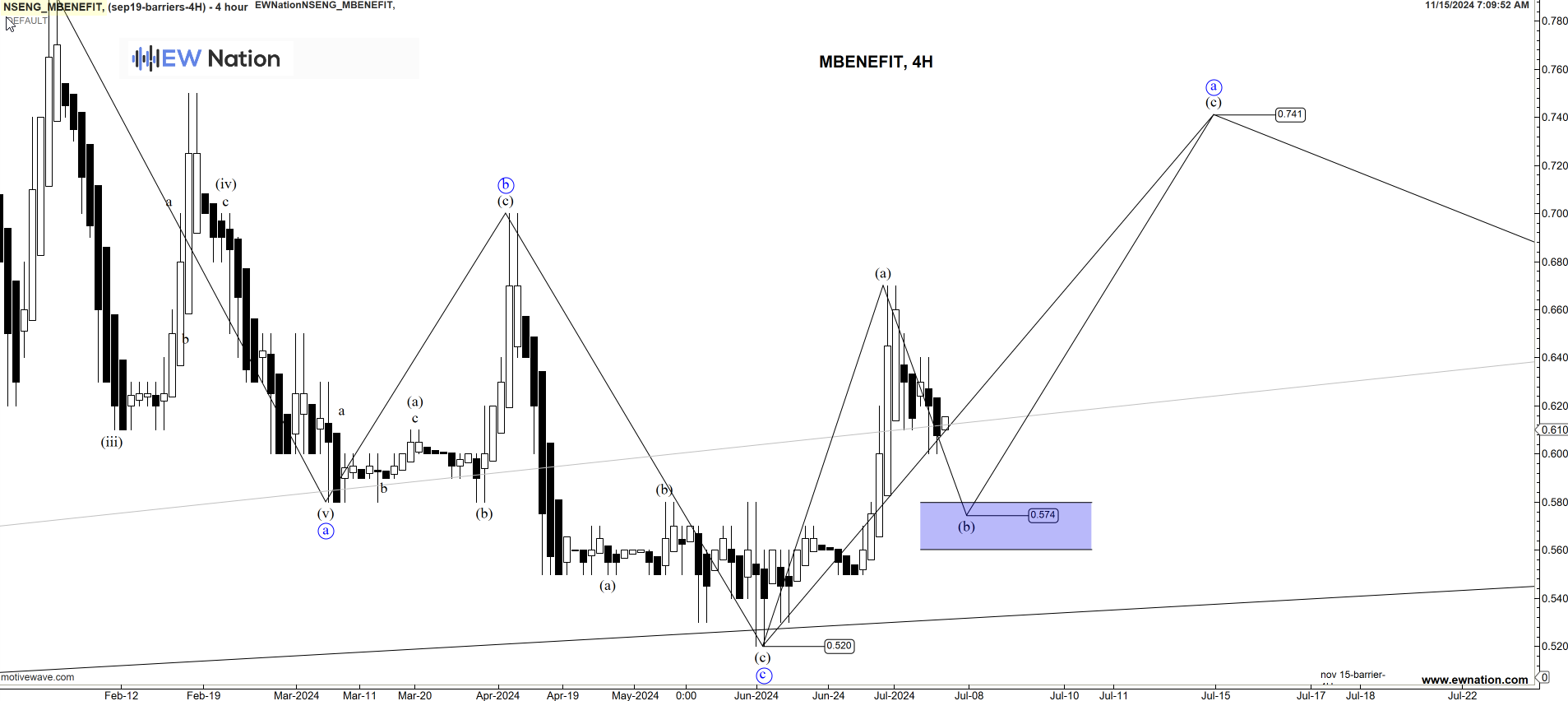

With MBENEFIT Elliot Wave Chart, the structure remains in a sideways correction. With the structure printing A-B-C of a corrective triangle, we expect that MBENEFIT will make progress towards the D-E to complete this barrier triangle pattern. Conversely, the move from 0.52 is expected to unfold in 3 waves with a target towards the 0.741 region for D.