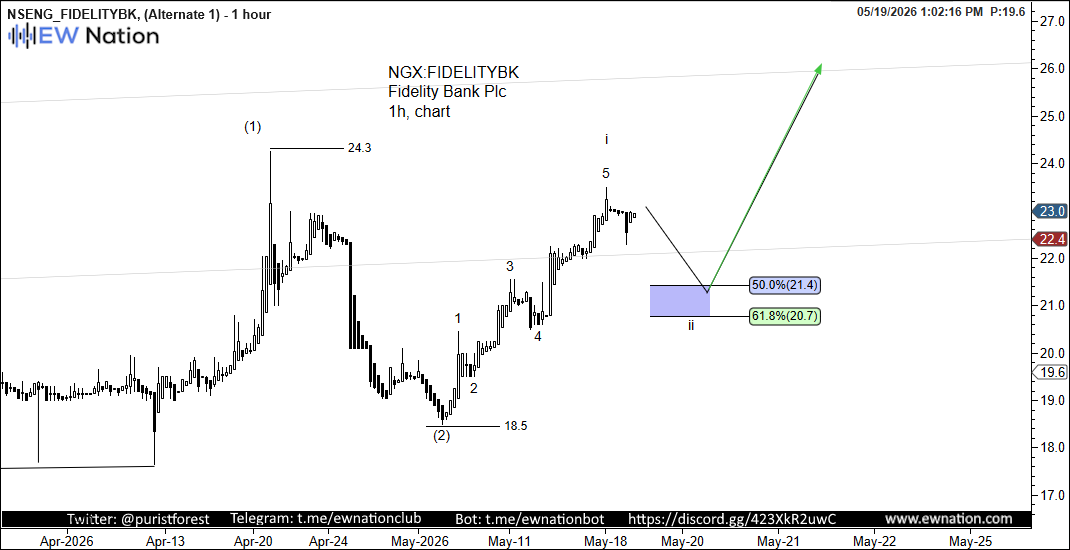

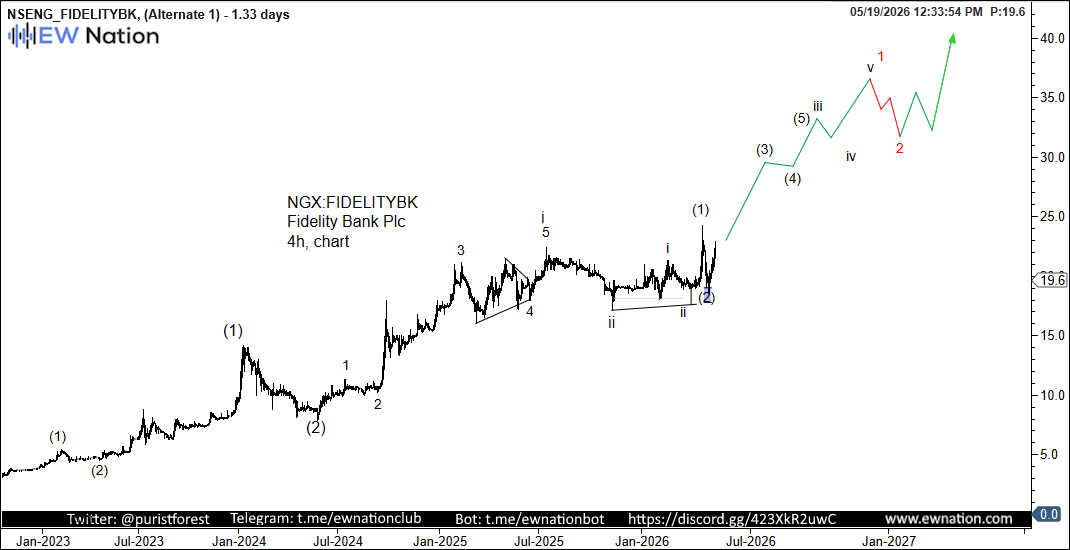

Bottom Line: Two Alternatives

5/19/26 12:09 EST (Last Price 22.95):

The impulsive looking bounce suggests that we may have reached the wave 2 bottom, the 1 hr chart shows that we may test the 21 lows again before further impulse.

📊 Fidelity Bank Plc (NGX: FIDELITYBK) — Latest Info

✅ Strengths

- Gross earnings rose 45.6% year-on-year to ₦1.52 trillion in FY 2025, while profit after tax reached ₦242.4 billion — underpinned by a 38.7% increase in interest income to ₦1.11 trillion and a 44.7% rise in fees and commission income to ₦113.4 billion. Total assets expanded 18.6% to ₦10.46 trillion and customer deposits grew 16.1% to ₦6.89 trillion, confirming broad-based franchise momentum rather than growth concentrated in a single income line.

- Fidelity Bank completed its CBN recapitalisation exercise in full, raising ₦259 billion through a private placement finalised in December 2025 and lifting eligible capital to ₦564.5 billion — above the ₦500 billion minimum for international commercial banks — elevating the bank to Tier-1 status. The capital adequacy ratio improved to 30.94% from 23.47% in the prior year, providing a materially strengthened buffer and unlocking balance sheet capacity for lending growth and regional expansion into 2026.

- Fidelity Bank serves over 9.1 million customers across 255 business offices and its UK subsidiary FidBank UK Limited, and has received multiple international recognitions including Euromoney's Best Bank for SMEs in Nigeria and BusinessDay's Export Financing Bank of the Year. With a dividend yield of approximately 11.9%, a five-year dividend growth rate of 44.27%, and a price-to-book ratio above 1 — one of only three Nigerian banks trading above book value — the stock offers an unusually rare combination of income, growth, and capital discipline for a mid-tier Nigerian lender.

⚠️ Risks

- Fidelity Bank carries approximately $556 million in forborne loans — primarily concentrated in the oil and gas and power sectors — and under a base-case provisioning scenario, its capital adequacy ratio could fall by as much as 394 basis points, the largest estimated impact among major Nigerian banks. While the FY 2025 CAR of 30.94% provides headroom, this forbearance exposure represents the single biggest latent risk on the balance sheet, and any CBN-mandated accelerated provisioning would compress both reported profits and distributable capital simultaneously.

- Half-year 2025 profit of ₦132.3 billion fell short of the ₦159.8 billion recorded in H1 2024, dragged down by ₦59.78 billion in derivative losses — a reminder that the bank's earnings profile carries meaningful mark-to-market volatility from financial instrument positions that can move sharply with exchange rates and interest rates, and that FY 2025's strong full-year result masks a more uneven intra-year earnings trajectory than the headline PAT suggests.

- Despite completing its recapitalisation, the CBN's June 2025 directive suspending dividend payments for banks with forbearance exposures creates uncertainty over future income distributions — and Renaissance Capital has warned that banks like Fidelity, which still needed to raise additional capital during the year, may have been forced to issue shares at lower valuations, introducing dilution risk. Net loans and advances also declined 2.4% year-on-year to ₦4.28 trillion as customers paid down maturing obligations, raising questions about loan book growth momentum heading into a high-interest-rate 2026 environment.