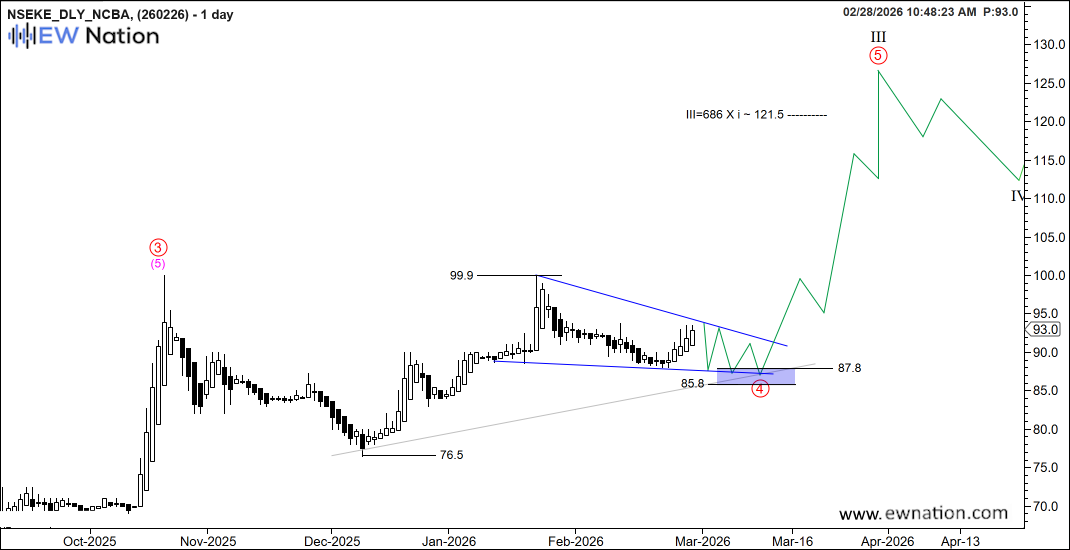

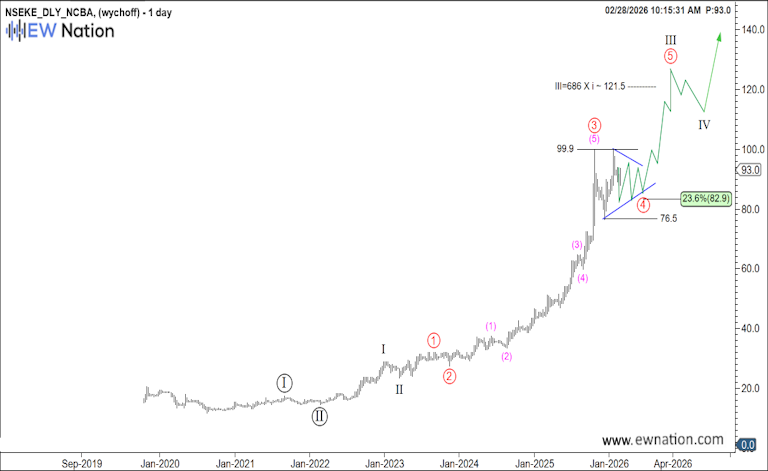

Bottom Line: Higher to complete wave III

2/23/26 05:55 EST (Last Price 93):

We are looking for evidence that wave 4 is complete such as a five wave advance above 99. We anticipate a further test of 87 region before advance.

2/23/26 05:55 EST (Last Price 93):

We are looking for a wave 5 completion, we anticipate a short run once 430 key level is broken for wave 5. Thereafter, wave 4 deline setting stage for wave 5.

Summary

Across Africa, traditional banking has leapfrogged into mobile-first financial services. Digital lending — instant, app-based loans delivered via mobile phones — is reshaping how banks grow, manage risk, and serve customers.

Africa’s banking environment differs from developed markets in key ways:

High mobile penetration

Large underbanked population

Informal income structures

Limited physical branch access in rural regions

Digital lending solves these constraints by using:

Mobile phone data

Transaction histories

Alternative credit scoring models

This enables near-instant credit decisions — often in minutes.

NCBA Group PLC offers a compelling case study of how digital transformation can drive both financial inclusion and profitability.

NCBA Earnings & Growth Data (2024–2025)

🔹 Full-Year 2024 Results

Profit after tax: KES 21.9 billion (up ~2% YoY).

Operating income: KES 62.7 billion.

Operating expenses: KES 32.2 billion (up ~10.6% YoY).

Final dividend: KES 3.25/share (KES 5.50 total).

NPL ratio: 11.2% of total loans.

Impairment coverage: ~60%.

These numbers show steady profitability with disciplined credit provisioning — a sign of strength in a challenging operating environment.

Digital Lending as a Growth Engine

Digital Loans Disbursements

Full Year 2024: > KES 1 trillion in digital loans disbursed; up ~+23% vs prior year.

H1 2025: KES 646 billion digital loans, +35% YoY growth.

Q1 2025: KES 307 billion digital disbursements, +32% YoY.

Q3 2025: Digital lending remained above KES 1 trillion, up ~35% YoY.

Insight: Digital lending now accounts for a substantial share of NCBA’s loan book growth and customer engagement. The Y-o-Y increases indicate rapid adoption among retail and business borrowers.